If you closed 25 deals in 2022, you're tracking toward 17 this year. Same listings, same sphere, the same hours invested. Different market.

You can feel the squeeze in the numbers, and not just because the closings are slower. Gas is up. Marketing platforms are up. MLS dues went up again in January. Your E&O carrier raised premiums. Your CRM raised seats. The written buyer agreements required since August 17, 2024 added paperwork to every showing. The deals you do close take more work to get to the finish line than they did three years ago.

The one number that hasn't moved is the share your brokerage takes off the top of every closing. Same percentage, same cap, same monthly desk fee whether you're crushing it or just hanging on. You're doing more work for less money, and a meaningful piece of what you did earn went somewhere that didn't earn it.

This post is about that piece. What it adds up to at producer volume, and what the structural alternatives actually look like once you run the numbers.

The setup

The working scenario: a Utah producer at a $500K average sale price, earning 3% commission per side. That's $15,000 in gross commission per closing.

The three brokerage models below are the ones most producing Utah agents actually work at today:

- Traditional split with cap. A 70/30 or 65/35 split where the brokerage takes its share until you've paid the cap (typically $20,000–$25,000 annually), then you move to 100% for the rest of the year. Most agents at major franchise brands.

- High-cap split brokerage. An 80/20 split with a lower cap (around $16,000) and a per-transaction fee after cap. The variant that grew fast in the last decade.

- Flat-fee. A single per-transaction fee, the same on every deal, every year, with no monthly desk fee and no cap to climb. Realty HQ's model.

Three scenarios for each: a 12-deal year, an 18-deal year, and a slow 8-deal year. The slow year matters more right now than it has in a decade.

The 12-deal year (steady volume)

Twelve deals at $500K average puts $180,000 of gross commission through your hands before any brokerage costs come out.

Traditional split (70/30, $25K cap): You pay 30% of every commission until reaching the cap, which hits after about 5.5 deals. The broker walks away with $25,000 from the cap, plus a $200 monthly desk fee that runs all year, plus modest per-transaction fees after cap. Annual cost: roughly $28,000.

High-cap split (80/20, $16K cap): You pay 20% until paying $16,000, which happens around deal 5.3. After that, a $285 transaction fee per closing, plus an $85 monthly fee, plus an annual tech contribution around $750. Annual cost: roughly $20,000.

Flat-fee (Realty HQ): 0.25% of the sale price, every deal, every year. At $500K average, $1,250 per closing. Twelve closings, no monthly fees, no cap. Annual cost: $15,000.

At 12 deals, you keep about $13,000 more at flat-fee than at a traditional split, and about $5,000 more than at a high-cap. The math favors flat-fee, but not dramatically. That changes in a slow year.

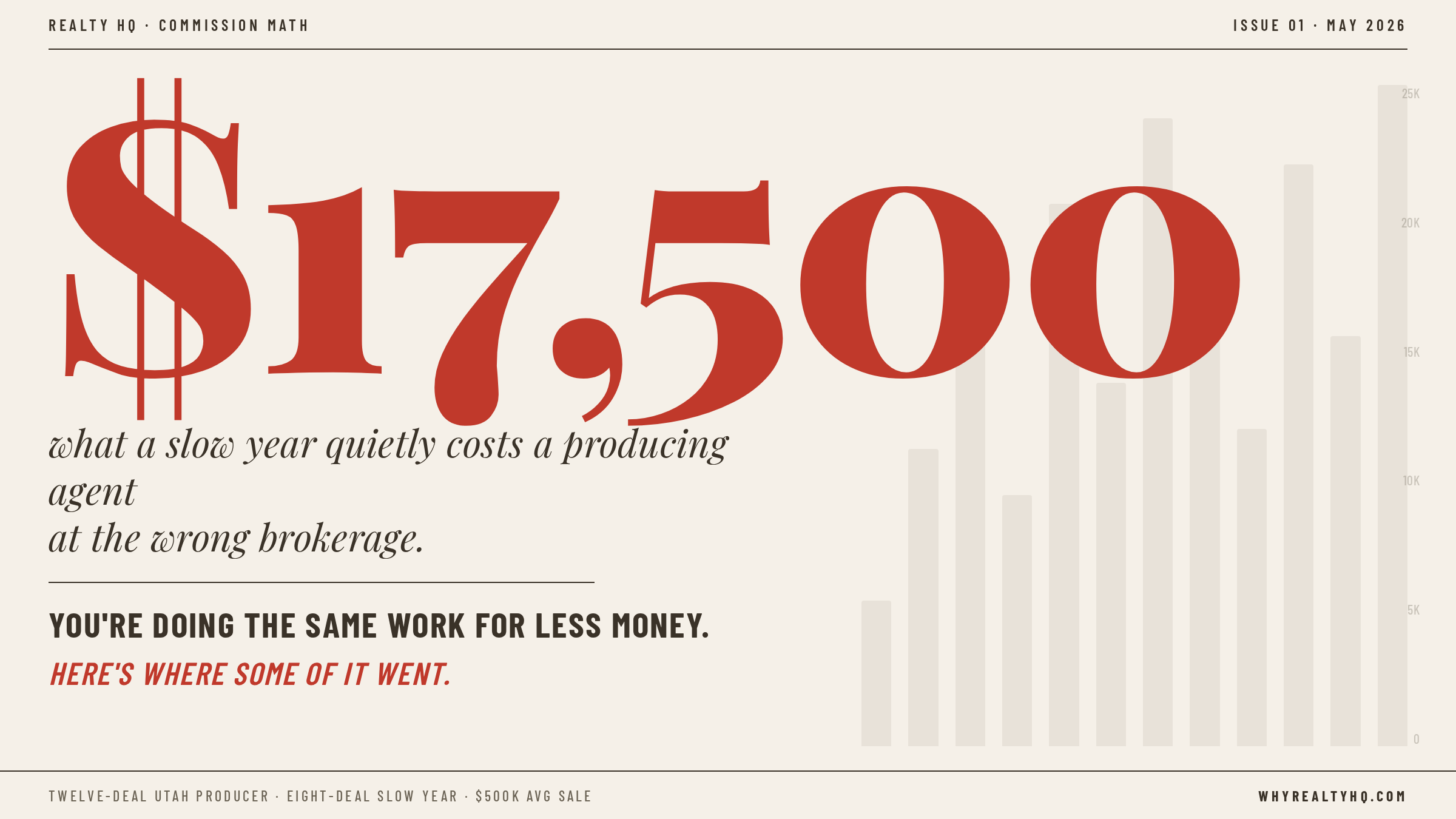

The 8-deal year (the slow year this market is producing)

Same agent at the same brokerage, having a tougher year. Eight closings at $500K = $120,000 in gross commission.

Traditional split: The cap is still $25,000. Whether you do 8 deals or 28, the cap is what it is. You hit it at deal 5.5, same as a 12-deal year. Annual cost: roughly $27,500. You paid the same brokerage cost in a slow year as in a steady year, except now it represents 23% of your gross commission instead of 15%.

High-cap split: Cap is $16,000, hit at deal 5.3. After that, transaction and monthly fees. Annual cost: roughly $19,000. Same dynamic. The brokerage cost is essentially fixed regardless of how the year unfolds.

Flat-fee: $1,250 × 8 deals = $10,000. Zero monthly fees, zero annual obligations. The brokerage cost scales with what actually closed.

This is the structural difference most agents never see until they're in a slow year. At cap-based brokerages, you prepay your worst year every cap cycle. At flat-fee, you only pay for the deals that actually close. In a market like this one, that's not a hypothetical.

At 8 deals, you keep about $17,500 more at flat-fee than at a traditional split. Same brokerage cost, fewer deals to absorb it.

What about the 100% commission shops?

There's a category that deserves honest treatment. The "100% commission" model that several Utah brokerages run is different from both the splits above and from flat-fee. Most charge a monthly desk fee ($300–$500), a per-transaction fee ($295–$495), and a handful of annual fees for E&O, tech, and compliance.

At low fees and tight operations, this model can come out slightly ahead of flat-fee on raw math at producer volume. The trade-off worth knowing: broker accessibility varies widely across these shops. Some have a working principal broker you can reach directly; others route you to a compliance team or a help desk when a contract goes sideways. The "tools" plan is tiered. The monthly desk fee charges the same in your slow month as in your peak month.

That trade-off is your call. We compare honestly because most brokerage recruiting content doesn't.

The structural case

The math at producer volume lands within a few thousand dollars across most of these models. The structural differences are what compound over time: no cap cycle eating into every reset stretch, no monthly fee running during slow months, one number on every deal with nothing added, and a working broker you can reach when a contract needs saving at 9 PM on a Sunday.

The urgency trigger

If you're at a cap-based brokerage, the stretch from your cap reset date through hitting cap again is the most expensive part of your year. At most major franchise brands, that reset is January 1, meaning right now you may be in the middle of it. Some brokerages run on an anniversary date instead — check your agreement either way.

Agents who switch in late spring or early summer get a full cycle at better math before the next reset would have hit them. Agents who wait until "next year" spend another full year prepaying their worst stretch.

The difference is somewhere between five and seventeen thousand dollars depending on how your year unfolds. A year of professional listing photography. A first hire. A down payment on an investment property. A real retirement contribution. Not life-changing, but not nothing. And it compounds.

The simple way to find out

Most producing agents at split brokerages have never run the actual numbers because the math is unpleasant to confront. The calculator at rhq-savings.netlify.app takes about three minutes. Plug in your actual deals, your actual average price, your current brokerage costs. The output is your number, not a marketing pitch.

If the number is small, you have your answer and you can stop thinking about this. If the number is large, you have a different question to ask.

The market isn't going to do you any favors next year. The brokerage cost is the one thing in your business you can change in May or June and feel the effect of immediately, on every closing for the rest of the year.

Lesley E. Mascaro, Principal Broker #5507521-PB00 | Realty HQ LLC, Brokerage #13775706-CN00